If you are looking to own a home of your own, under the Pradhan Mantri Awas Yojana (PMAY) scheme, there are only nine months left for you to arrange the amount for down payment, decide the location, builder and the home loan lender.

The recently introduced Credit Linked Subsidy Scheme (CLSS) for Middle Income Group (MIG) to be called CLSS for MIG will be for a period of one year starting 1.01.2017.

Let’s see who all are eligible for the MIG category, who all within a family can apply, how much is the subsidy in rupee terms and how does the subsidy impact the loan amount.

The middle-income earners

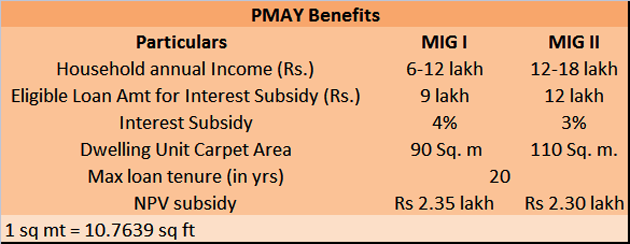

The new category MIG, introduced recently, will further comprise of two slabs. The Middle Income Group (MIG) – I will comprise of households having an annual income between Rs.6,00,001 up to Rs.12,00,000.

And, the Middle Income Group (MIG) – II will comprise of households having an annual income between Rs.12, 00,001 up to Rs.18, 00,000. So, effectively anyone earning between Rs 6 lakh and Rs 18 lakh per annum can avail the benefits of subsidized loans provided other conditions are met.

Who are all eligible?

The scheme is primarily aimed at providing housing for all. Therefore, understandably, all those who already own a home or any of their family member own a home, are kept out of the benefits of PMAY.

The rule says, “The beneficiary family should not own a pucca house and the beneficiary family should not have availed of central assistance under any housing scheme from Government of India.” A beneficiary family will comprise of husband, wife, unmarried sons and/or unmarried daughters. To avoid duplication, beneficiary family members have to provide their Aadhaar numbers while applying for the loan.

But, as per the guidelines, “An adult earning member (irrespective of marital status) can be treated as a separate household, provided that he/she does not own a pucca (an all weather dwelling unit) house in his / her name in any part of India.”

So, even if children (married or unmarried) are staying with their parents in a house owned by the parents (or on rent, in the same or another city), they can opt for PMAY provided they are earning and don’t own any other home.

For a married couple living on rent and even if their parents own a home, will anyhow is treated as a separate household. However, if they wish to avail PMAY benefits, they will be eligible for a single house, bought by either of the spouses or both together in joint ownership.

Subsidy

In the MIG – I category, individuals will get 4 per cent interest subsidy on a loan amount up to Rs 9 lakh, and in the MIG – II slab category individuals will get a 3 percent subsidy on a loan amount up to Rs 12 lakh. If one needs an additional loan, the lender will prove it but the additional loans beyond the subsidised loan amount will be at a non-subsidised rate.

How does it work

Say, someone in the MIG II category, wishes to buy a house costing Rs 60 lakh. After the mandatory minimum down payment of 20 percent i.e. Rs 12 lakh, the balance of Rs 48 lakh can be arranged through a loan. But under PMAY, a subsidy of 3 percent would be applicable till Rs 12 lakh, hence, the lender’s home loan interest rate will be applicable on the balance of Rs 36 lakh.

How is the subsidy adjusted

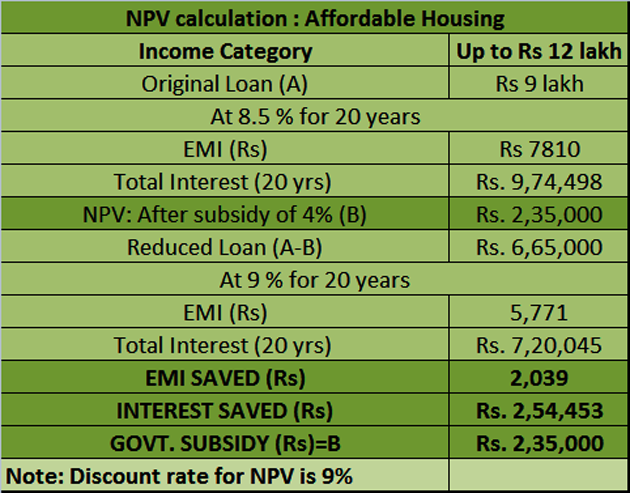

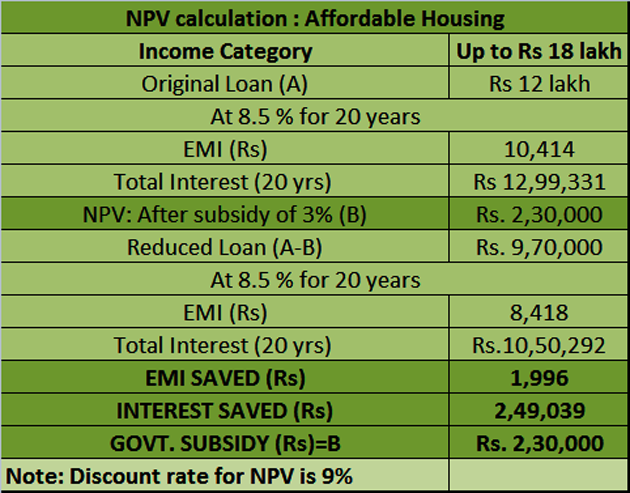

The interest subsidy amount will not be the differential of interest amount (of actual and subsided rate) but will be the net present value (NPV) of the interest subsidy amount. It is to be calculated at a discount rate of 9 percent. For calculating NPV of the subsidy, one will need the loan’s amortisation schedule as the interest portion of each equated monthly instalment (EMI) has to be considered. Thereafter, use the Fx function in an excel sheet to arrive at the NPV. Because of the subsidy amount, your loan amount reduces and, therefore, the interest burden to comes down.

Suppose on a home loan of Rs 12 lakh, the NPV of the 3% interest subsidy comes to Rs 2.30 lakh. So, out of the loan amount of Rs 12 lakh, the amount of Rs 2.30 lakh will get deducted and the borrowers has to pay EMI on the balance i.e. Rs 9.7 lakh at a rate at which the lender is providing loans, which could be 8.75 or 9 percent or whatever the MCLR based home loan rate is the bank.

The interest subsidy will be credited upfront to the loan account of beneficiaries resulting in reduced effective housing loan (deducting it from the principal loan amount) and Equated Monthly Installment (EMI). The borrower will pay EMI as per agreed document rates on the remainder of the principal loan amount.

Loans under PMAY

The PMAY benefits can be availed if one wishes to acquire a new house from the developer or the builder and even for buying a house from the secondary market through repurchase. One may also take a loan for the construction of the house.

Interestingly, if someone already owning a home wants to avail PMAY benefit, there’s still a possibility. The government has clarified that the Mission (Housing for All by 2022) also provides for enhancements/incremental housing to the existing ‘pucca’ house under the CLSS component. So, a home loan provider cannot decline or not entertain an applicant seeking a home loan for the addition of a room, kitchen etc to the existing dwellings solely on the ground that the applicant is already possessing a pucca house.

Home area

Under PMAY, the area of the house is different for all categories but it’s the carpet area that is to be looked at. For MIG I, the carpet area is to be 90 sq mt (968.752 sq ft) and 110 sq mt (1184.03 sq ft) for MIG II category. Carpet area is the area enclosed within the walls i.e. actual area to lay the carpet. This area does not include the thickness of the inner walls. If you add up outer walls, balcony and other common areas, it’s the built-up area.

Further, when space for lobbies, stairs, elevators etc is added, the super built-up area is arrived at. Builders as of today are charging buyers on the super built-up area, a practice which the RERA is going to remove by making the buyer pay only on the basis of carpet area.

A 110 sq mt (1184.03 sq ft.) carpet area is close to 1480 sq ft of the built-up area as nearly 25 percent or even higher, is the difference between them. A 2 BHK could look feasible in several locations. This new move has made affordable housing scheme accessible to many people living in urban areas now.

Subsidised loans from where

One can avail PMAY linked loans from any primary lending institutions such as scheduled commercial banks, housing finance companies, Regional Rural Banks s), State Cooperative Banks, Urban Cooperative Banks, Small Finance Banks, Non Banking Financial Company etc. There will not be any processing charge for eligible housing loan amount as per income criteria under the Scheme. For additional loan amounts beyond the eligible loan amounts for interest subsidy lenders can charge the normal processing fee.

The impact

PMAY scheme for MIG buyers may not push up the demand for residential housing much. The benefit of Rs 2.3 lakh/Rs 2.35 lakh may not appeal much considering the cost of houses in the urban areas. The government may consider doing away with the area restriction of 90/110 sq mt to pep up the demand.

Conclusion

Affordable housing has been given infrastructure status in Budget 2017, which should aid developers in takings its associated benefits. But for a common man, the timely delivery of the house still remains a distant dream. For availing the benefits, the builders had to complete the affordable housing projects in 3 years but now ( Budget 2017) have to complete in 5 years. Tread carefully and evaluate all the options before venturing out to explore the affordable housing segment, even if you are a first-time home buyer.

Courtsey: Sunil Dhawan | Economic Times | April 05, 2017